Looking forward: Canada's economy in 2021

Joe Brusuelas, Chief Economist, RSM US LLP

The North American economy is defined by two trading partners connected through a common set of sociopolitical values, culture and industry. For every Raptors fan, there’s a heartbroken Warriors fan. And for every Ian Tyson who thinks he’ll “go out to Alberta,” there’s a Neil Young living in Los Angeles. Is that American or Canadian R&B that The Weekend is selling?

Canadian output is likely to expand by roughly 4 per cent in 2021 and 2022.

Though Canada had been somewhat immune to the business cycle of the United States, the interconnectedness of the American and Canadian economies and their financial markets appears to have grown during the post-industrial era. In fact, one might make the case that it is one large integrated economy separated by two currencies.

We could point to the U.S. reliance on Canadian resources and the Canadian reliance on American refineries. The fact that auto parts can go back and forth across the border five times while being manufactured makes it difficult to label the final product as American or Canadian. In the digital economy, Microsoft has headquarters in Seattle and a campus in Vancouver. And with U.S. immigration in shambles, universities in Canada are finding it easier to attract intellectual capital.

So with the turmoil caused by U.S. trade war and the American election coming to an end, and with the coronavirus attacking indiscriminately on each side of the border, it is time to consider growth prospects for the year ahead and take stock of the condition of the Canadian economy.

A choppy and uneven outlook

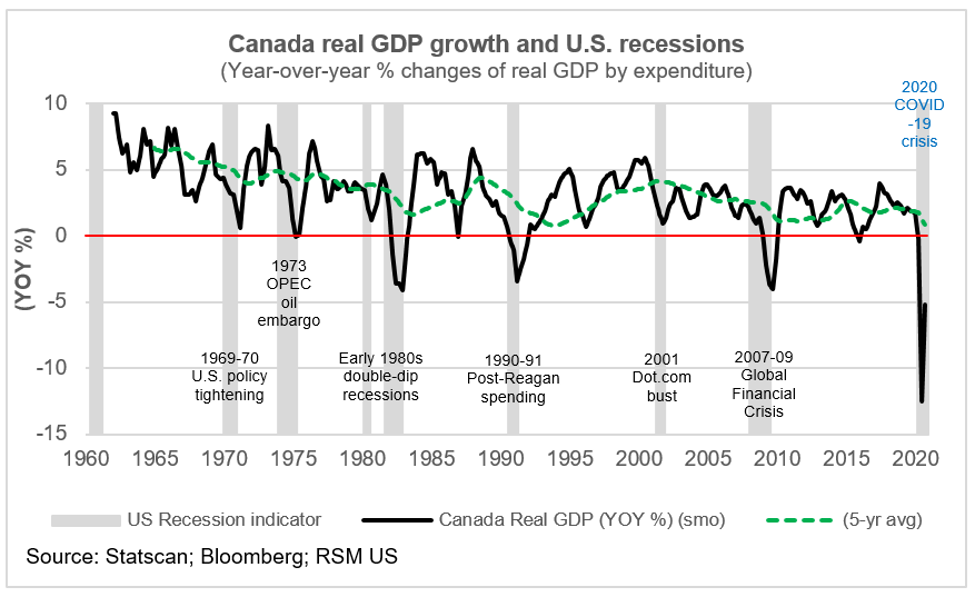

Canada’s economy has been decelerating since the end of 2017 and has been in outright decline for the whole of 2020. Prospects for recovery and expansion in 2021 are directly linked to an equitable distribution of a safe and effective vaccine.

Canada’s total output declined by 12.5 per cent and 5.2 per cent in the second and third quarters relative similar periods in 2019.

Once that vaccine is in place, we are confident that the reopening of the domestic economy coupled with a reduction in trade frictions in North America will combine for robust growth over the next two years. For this reason, Canadian output is likely to expand by roughly 4 per cent in 2021 and 2022. While this is solid, the Canadian economy is not likely to reach its full capacity to produce until 2023.

Canada’s total output declined by 0.3 per cent in the first three months of 2020 relative to the first quarter of 2019, followed by declines of 12.5 per cent and 5.2 per cent in the second and third quarters. Note that we are referring to year-over-year percentage changes in real gross domestic product, which are more valid indications of economic growth during periods of economic stress than the outsized annualized numbers mentioned in the press.

All in all, the third quarter was not as bad as the second quarter. But that’s like saying that a five-car pileup is better than a 12-car pileup.

And that’s not to say that the economy can’t or won’t improve, though the rates of change might not be as dramatic as after the initial shock to the economy. Monetary policy is in place and fiscal programs are propping up the income of Canadian households. So the likelihood of another economic or financial collapse will likely depend on the time it takes to vaccinate the entire population.

As Tiff Macklem, governor of the Bank of Canada, told the House of Commons recently, “the very rapid growth of the reopening phase is now over” with the economy entering a “slower-growth recuperation phase.” For 2020 as a whole, the bank anticipates “that the economy will have shrunk by about 5½ per cent,” he added.

Because some parts of the economy will not be able to completely reopen until a vaccine is widely distributed, the bank expects “annual growth to average almost 4 per cent in 2021 and 2022,” anticipating uneven gains “across sectors and choppy over time,” he said. There are other factors at play. For example, the bank expects that the energy-intensive parts of Canada “will face greater difficulties than others,” he said.

The bank expects business investment to remain subdued and exports to grow only slowly, and concludes that “the economy will still be operating below its potential into 2023,” Macklem said.

Decreases in potential output

The economies of the U.S. and Canada have endured large supply shocks that will likely leave both economies reeling for a number of years. Damages to the labour force and a decline in investment in productivity will result in output below what the economy is capable of producing.

Because of the pandemic, the Bank of Canada’s estimates for the growth of potential GDP – excluding containment effects — have been halved since April. From potential output growth of 1.8 per cent per year in 2019, the bank now estimates potential output growth falling to 0.7 per cent in 2020 and 0.9 per cent in 2021, before leveling off at 1.1 per cent to 1.2 per cent per year in 2022-23.

The International Monetary Fund projects that it will take six years before the economy is operating at its potential. The output gap — defined here as the (ratio of) the difference between actual GDP and potential GDP – has plunged to greater than 3 per cent only three times since 1980. It occurred during the 1980s double-dip recession after a series of energy shocks, then during the 2008-09 Great Recession after the financial crisis, and, finally, this year during the aftershock of the economic shutdown and equity market crash. In the first two of those devastating economic downturns, it took five to six years for the Canadian economy to close its output gap, and we expect no different with the most recent shock.

Considering that the output gap might not be closed until 2025, and that potential GDP will be growing at a reduced rate, then the Bank of Canada’s forward guidance of low-for-long interest rates seems more than appropriate.

With an accommodative monetary policy in place, the fiscal responses of the U.S. and Canadian governments will determine the extent of damage to the economies of the trading partners as well as the length of time until recoveries in each of the economies reach sustainable rates of growth.

Long-term labour-market stress

As with the overall economy, the labour market has undeniably improved since the outbreak of the pandemic. There were 2.9 million fewer jobs in April 2020 than there were in April 2019. By October, there were 600,000 fewer jobs than in October 2019.

The bulk of those losses remain in the service sector, where half a million people are still without a job. That implies that typical shovel-ready infrastructure programs — which are of greatest value to the construction sector — might fall short in restoring the overall labour market to pre-pandemic levels.

Indeed, if the pandemic were to permanently change the way we work and how we shop and entertain ourselves, then the economy runs the risk of a shortage of jobs in the service sector. An oversupply of labour would have the effect of dragging wages downward and reducing household income and consumption. Reduced spending by the consumer sector would have a profound impact on economic growth.

Policies to address service-sector employment could focus on education of the labour force, not just in terms of academic advancement, but also in acquiring additional skills through apprentice programs and trade schools.

The body of research following the financial crisis in 2008-09 — and the U.S. government’s truncated response to the Great Recession — found a degradation of the U.S. labour market during the long, drawn-out recovery.

Skills among unemployed workers deteriorated as they found themselves unable to keep up with changing technology. The unemployed who were unable to quickly rejoin the labour force were stigmatized as the duration of being unemployed lengthened. This resulted in a cycle of diminished productivity and a degradation of potential output.

April’s sudden decrease in the duration of Canadian unemployment and the subsequent increase above its long-term average in August – like annualized GDP growth — need to be interpreted first in the context of the shock caused by the economic shutdown and then by its potential for long-term negative effects.

In April, the economic shutdown caused a significant number of workers to join the ranks of the unemployed all at once. As the economic hardship mounted through the summer and into the fall, the average duration of unemployment moved above its average from 2000 to 2019.

The trend in duration during the upcoming vaccination program should be an indication of the need to maintain public assistance.

The consumer sector

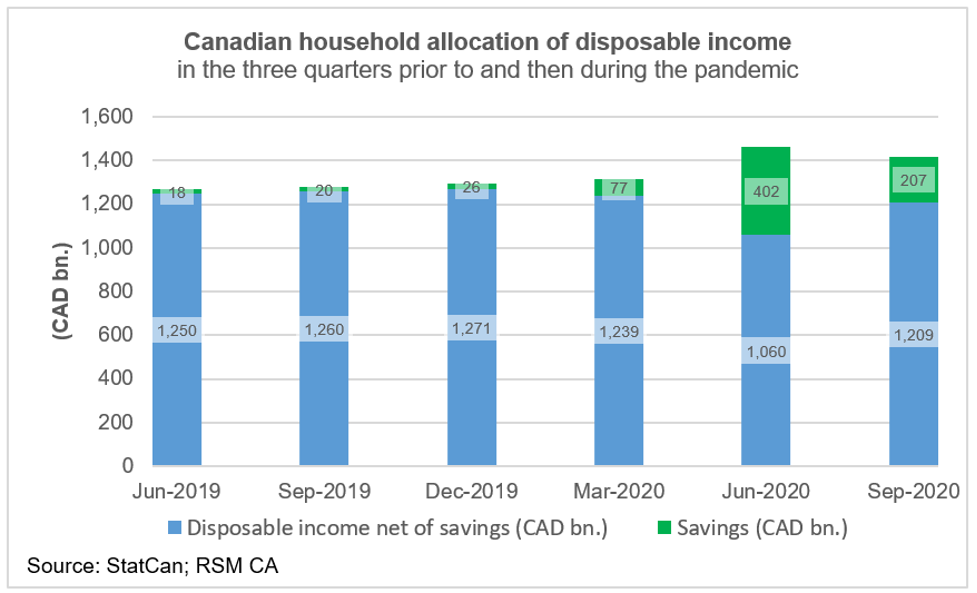

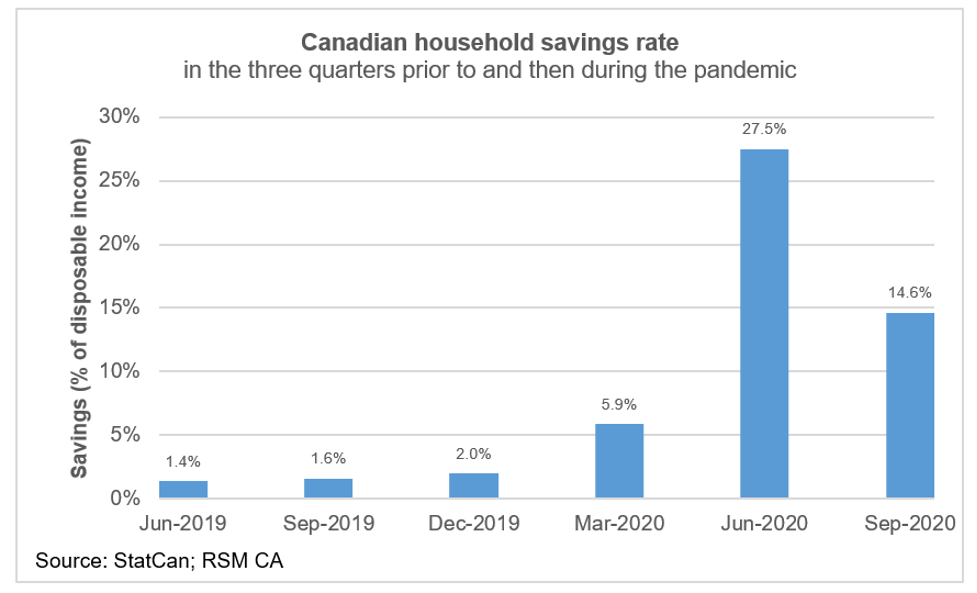

In the third quarter of the pandemic, households continued to exhibit an increased propensity to save despite increases in disposable income.

In the three quarters before the pandemic, households were allocating 1.4 per cent to 2.0 per cent of disposable income to savings. While that’s great for the housing market and the retail and wholesale sector, the lack of savings and the burgeoning amount of household credit has always been a concern for the Bank of Canada’s interest-rate policy decisions.

In the three most recent quarters, household savings soared to 5.9 per cent in March as the novel coronavirus set in, then to 27.5 per cent in the June quarter and 14.6 per cent in the quarter ending in September. Within the perversity of the pandemic, an increase in savings could become a concern for the fiscal authorities should the lack of household spending turn a supply shock into a demand shock.

Again, this will depend how quickly vaccines are distributed and how long they retain their efficacy.

The corporate sector

Financial firms probably have the monetary authorities to thank for the shallowness of their downturn – if there was one — and the return to normal levels of net operating surplus. One would suspect that the corporate sector will lead the economy out of the recession just ahead of a distribution of a vaccine in mid-2021.

Nonfinancial corporations made a remarkable recovery in the third quarter and are 98.5 per cent of the way back to normalcy going into the last three months of the year. Moreover, as trade barriers with the U.S. decline, we think that the nonfinancial corporations are poised for outperformance as the economy of its neighbor to the south begins to awaken.

The Bank of Canada and financial conditions

Economists have come to understand that monetary policy and economic shocks are transmitted to the real economy through the financial system. As such, monetary policy decisions to create an accommodative environment for investment will entail the confidence that the central bank will respond to supply or demand shocks or shocks to the financial sector. They will also entail the confidence that the setting of interest rates will be appropriate for the level of economic activity and inflation.

Since the 2008-09 financial crisis, the U.S. and Canadian central banks allowed interest rates to rise once the economic recoveries from the crisis were sustainable. They then pushed interest rates back to the zero bound when economic growth was threatened by the 2014-15 oil glut and commodity-price collapse and then by the ill-advised trade war in 2018 and, more recently, the pandemic.

The Bank of Canada’s policies of near-zero overnight rates and large-scale purchases of longer-term securities correspond to the standards of a Taylor Rule response function. (The Taylor Rule determines the appropriate level of a central bank’s policy rate, according to the deviation of inflation from the bank’s target for inflation, and by the level of employment relative to what is considered to be a noninflationary level of employment.)

Although the Taylor Rule would suggest negative interest rates in Canada and the U.S., there are risks that the economies might never recover normal levels of growth, as is the case in Japan. This could occur if the confidence in the sustainability of an economic recovery and if higher price levels are undermined, or if the existence of negative returns on fixed-income investments were to create bubbles in other assets (such as speculation in the housing market or equity market).

We would argue that the Bank of Canada and the Federal Reserve have made the right choices, most of the time, and provided the correct forward guidance. The Bank of Canada’s balance sheet has stabilized, with buying longer-maturity bonds reducing costs for residential fixed-rate and corporate borrowing. “Canadians can be confident that borrowing costs are going to remain very low for a long time,” Macklem, the Bank of Canada governor, said.

In fact, the bank consulted with market participants who thought the Bank of Canada’s Government Bond Purchase Program (GBPP) “was the key factor in raising the unprecedented amount of long-term federal government debt in an orderly manner, since the GBPP absorbed a significant portion of the extra issuance,” the bank said in its summary of its findings.

The consensus from the market was that “the 10-year sector could readily absorb more net issuance since the sector benefits from liquid and well-developed futures markets,” the summary said.

As such, financial conditions in Canada are accommodative, with the only potential source of stress coming from the equity markets and the potential for OPEC-induced disruption.

Of note, there has been an increase in oil prices, which might have more to do with OPEC’s successful reduction of supply than with diminished demand for energy during the pandemic. Still, the reduced number of North American oil rigs and the increased number of bankruptcies in the energy sector might suggest otherwise were the pandemic’s effect on household consumption to continue much further.

Coronavirus update: Cases, deaths and vaccines

The devastating resurgence of the novel coronavirus in the U.S. will undoubtedly threaten the economy of Canada through the trade channel. Its resurgence in Canada follows a similar autumn trajectory, with the cumulative number of cases surpassing 400,000 at a rate of 6,200 newly reported infections per day in early December. That is nearly three times the peak rate during the first wave in early May. Deaths are occurring at a rate of 86 per day, and have been increasing since October.

The hopeful news is that the vaccine appears to be near. England has recently authorized use of the Pfizer vaccine, and Maclean’s reports that “Ottawa hedged its bets by making advance-purchase agreements for a wide portfolio of vaccine candidates.” These include three versions of the vaccine, with prospective releases in the coming weeks, according to Maclean’s:

Pfizer/BioNTech (U.S.) – “Canada has an advanced-purchase agreement for 20 million doses, with the option to buy 56 million more. Since it is a two-dose vaccine, the initial order would be enough to vaccinate 10 million Canadians.“

Moderna (U.S.) – “Fully 20 million doses, with the option to purchase 36 million more. The initial advance order would be enough to vaccinate 10 million Canadians.” Regarding fears that other countries might get the vaccine before Canada, “Moderna’s chief medical officer told the Globe and Mail that doses of the first batch will be coming to Canada—albeit a small amount; he is ‘hopeful that you’ll see significant quantities coming to Canada’ ” in the first and second quarter of 2021.

AstraZeneca/Oxford (U.K.) – “Canada signed an agreement in September for 20 million doses,” Maclean’s reported. The report continued: “The director of the Oxford University vaccine group called this the ‘vaccine for the world.’ That’s partly because it’s low cost — about US$3 per dose, one fifth that of the Pfizer and Moderna vaccines — and because it can be stored at the temperature of a common refrigerator.”

For more information on how the coronavirus is affecting midsize businesses, please visit the RSM Coronavirus Resource Center.

This article was reprinted with permission from The Real Economy Blog - Dec. 9, 2020. To view the article online, please visit https://realeconomy.rsmus.com/looking-forward-canadas-economy-in-2021/